Contribute

| Will Inflation Deflate Your Retirement? |

Press Release

08/26/2021

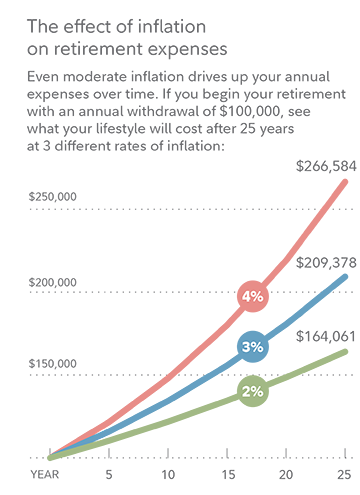

Concerns about rising inflation are everywhere. If you're already retired and living off your investment income, you may be especially worried, regardless of the size of your nest egg. Will your retirement plan be able to withstand higher prices? For how long? And how high will inflation go? Will it add to the volatility in the stock market? Will it prompt the Federal Reserve to raise interest rates sooner than expected? Perhaps most important, will it impact your lifestyle? For now, even experts have more questions than answers about how high inflation will go, and what it means for the economy—and you. That's because inflation is made up of various components, some driven by short-term, pandemic-related factors and others that have been long-standing, like the rise in health care costs. "Nobody knows exactly what's going to happen because we've never been in this situation before," says Claus te Wildt, senior vice president of capital markets strategy at Fidelity. "We have all these factors coming together and no historical comparison. We don't know yet how this is going to play out." While there are no certainties right now, Fidelity professionals do have an outlook on inflation based on market analysis and historical comparisons that is used to inform portfolio management. "Market indicators suggest that over the next 20 to 30 years, inflation will be somewhere between 2% and 3%," says Jake Weinstein, a research analyst with Fidelity's asset allocation research team. "And while there are more forces that suggest inflation could run higher than run lower, we don't expect a return to 1970s-like hyperinflation." Because financial plans work within ranges of possibilities, they are designed to withstand bumps in the road. Fidelity's target asset mixes for managed portfolios currently assume 2.5% inflation when assessing retirement goals. (For more detail on Fidelity's analysis, see our quarterly market update.) Here's how having a diversified investment plan—and the appropriate insurance and estate planning strategies—can help address some of your top concerns regarding rising prices and your lifestyle and legacy. Most retirees already have some inflation-adjusted protection through Social Security, and some may have inflation-adjusted defined benefit pensions or annuities with cost-of-living adjustments. If you assume that inflation will average 2% to 2.5% in the upcoming years, your investment goal would be to earn a return of at least that much or greater. If you think inflation is going to go up beyond that—either temporarily or long term—you may want to consider inflation-resistant investments for your portfolio and diversify across asset classes to help reduce inflation risk further. "Because most economists don't foresee an extremely high level of inflation lasting for years to come, you don't have to drastically change your allocations if they are already diversified," says Naveen Malwal, an institutional portfolio manager at Fidelity's Strategic Advisers LLC. "For example, within our clients' accounts, we currently have modest exposures to investments that have historically done well when inflation has been rising." Here are some options included in Fidelity managed account portfolios that individual investors can consider: And if the inflation outlook radically shifts higher because of unforeseen circumstances? The same strategies would still apply. "As long as you are diversified, you'll be doing all you can to hedge risks to inflation," says Weinstein. Do keep in mind that diversification and asset allocation do not ensure a profit or guarantee against loss. If you think your retirement lifestyle is going to cost more in the future because of inflation, your instincts might be telling you that you need more cash available for everyday expenses. For some retirees, that cash allotment is just a few months of spending, or maybe the amount needed yearly as a required minimum distribution from their IRA or 401(k) accounts. For the more conservative, it could amount to a few years of living expenses or more, depending on how they feel about the potential for withstanding a market downturn. But assuming you have a solid cash plan in place now, you might want to consider doing just the opposite if you are particularly worried about inflation: Hold less cash and invest for growth potential. "Unless our assets are growing at the same rate as inflation or greater, we're going to feel like we can't afford as much a few years from now," says Malwal. "Adding more to cash could leave you more exposed if that cash is not keeping up." Jennifer Wines, a Wealth Management Advisor for Fidelity, has a client who has kept a great deal of his holdings in cash ever since retiring. The current inflationary environment is making him rethink his conservative strategy, because even if the cash is not intended to cover his living expenses, he still wants to preserve his capital with the hope of leaving the legacy he wants to his heirs and charity. "Nobody wants to have their purchasing power eroded—not even somebody who has millions of dollars above and beyond what's needed to live their life comfortably," says Wines. Rising costs for a trip to Hawaii are one thing. Rising costs for prescription drugs and hospital care are on another level. Health care costs have been rising faster than the rate of inflation for years, and will likely continue to do so. Fidelity estimates that an average retired couple age 65 in 2021 may need approximately $300,000 saved (after tax) to cover health care expenses in retirement. And about 70% of those aged 65 and older will require some type of long-term care services.* Depending on your needs and your financial situation, you might want to consider long-term care insurance. "Even if you think you have enough to cover the costs involved, you may have to lower your standard of living or adjust what you plan to leave to heirs in order to spend more on health care, especially if that care is going to run higher than the industry averages," says David Peterson, head of wealth planning at Fidelity. You might also want to assess your life insurance and disability insurance needs, especially if you are still working in retirement in some capacity and count on that income to cover your spending. Even if your personal purchasing power isn't really affected by inflation, you may still be worried about the overall economy. If the stock market falters or the economy snags, it could affect your overall wealth and limit what you can leave to heirs or charity. This is the kind of worry that Viktor Misko, a vice president, wealth planner at Fidelity, is hearing a lot of right now, with inflation worries mixed in with concerns about the markets and the changing tax and estate planning landscape. The headlines are hard for people to ignore, and the COVID-19 pandemic has changed people's priorities and made them worry about all sorts of things. "Almost every conversation begins and ends with some level of uncertainty. I focus with clients on what we know and what can impact their own financial plans," Misko says. Because estate planning is by nature a long-term process, there are multiple factors that may have an impact on it, including inflation concerns. As a result, an estate plan should be constructed in a flexible enough way so that the plan can adapt to changes while still accomplishing a client's goals. A plan that is too restrictive may require more frequent updating (with the associated legal expenses) or risk not being as successful as originally intended. Inflationary concerns and the potential impact on the overall economic environment may ultimately prove to be less influential than, for example, a potential change in estate tax law. "The key is to not make short-term decisions," says Misko. "If you're worried about what lies ahead, you can be proactive about it, and make changes that might fit a number of potential scenarios." Whatever direction inflation eventually goes, the key is having a plan that can enable you to live the life you want. Working with a professional can help you find the strategy that works for you. Your attorney and tax professional can help you consider changes consistent with your unique situation.Key takeaways

Should I change my mix of investments?

Should I have more in cash or less?

How can I insure against the unknown?

Will inflation limit my legacy?

You may also access this article through our web-site http://www.lokvani.com/