Contribute

| Unretirement: The Financial Implications Of Working Longer |

Jai M. Dev

08/25/2015

A growing number of people plan to work past traditional retirement age, and not for the reasons you might suspect. Here are three key questions to ask yourself if you're planning to extend your career.

More than half of respondents surveyed in the Retirement 2.0SM study by Ameriprise Financial plan to retire gradually by working less or consulting.¹ While some plan to stay on the job for financial reasons, far more say they will do so to stay mentally and socially stimulated, according to the study. As Chris Farrell, Senior Economics Editor for American Public Media's Marketplace and author of Unretirement, writes: "The tantalizing promise of unretirement for younger generations is realizing that they will have much more time to better merge their careers and the search for meaning, to pursue job flexibility and creative variety, over a lifetime."

So what should you consider if you plan to keep working?

1. Will you need to supplement your income?

"The first thing to ask is: Will you need to replace 100% of your current income, or will you be able to scale back?" says Dennis Mashuga of Financial Planning Advanced Advice at Ameriprise Financial. "Many can reduce their costs of living after leaving regular employment, but you'll want to sit down with your financial advisor and work through different scenarios."

If you end up working part time, consulting or starting your own business, you can still draw on your retirement savings to supplement your income. "As long as you are 59½ or older, there are no tax penalties for taking distributions from your retirement portfolio," Mashuga says.

In addition to perks such as health insurance and paid time off, staying on with a company can also have long-term benefits. "If you continue to work at your current employer or roll your 401(k) plan to another employer with a compatible retirement plan, you don't have to take your required minimum distribution, which is usually required at age 70½," Mashuga says. This means your retirement portfolio can continue to grow until you are ready to retire.

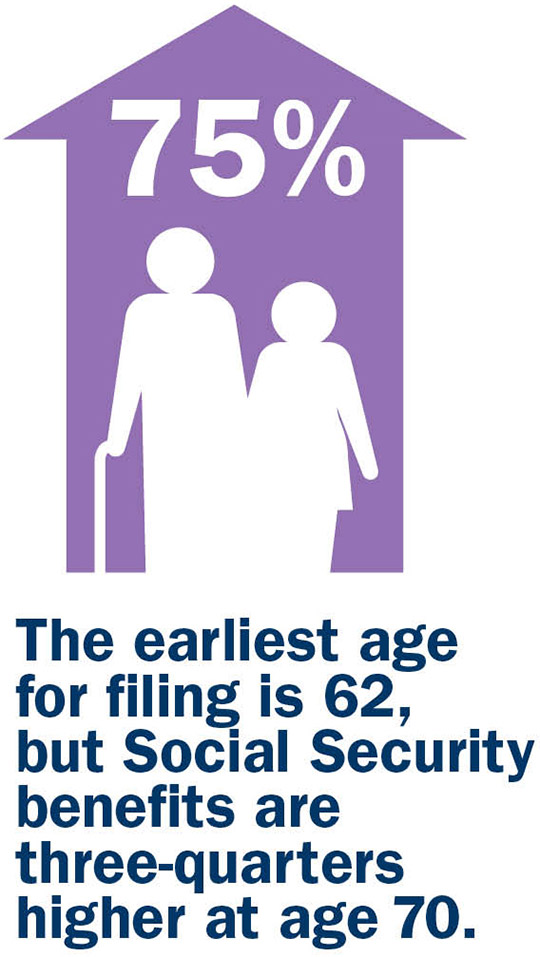

2. How will it impact your Social Security?

If earning an income allows you to delay taking your Social Security, the payoff can be considerable. According to the Social Security Administration, benefits are more than 75% higher at age 70 than if you begin collecting at 62 (the earliest age you can file). If you decide to take Social Security to supplement your unretirement income prior to the full retirement age of 66, keep in mind that doing so could reduce your benefit. For example, if you're younger than 66 during all of 2015, $1 will be deducted from your Social Security benefit for each $2 you earn above $15,720 — otherwise known as "excess earnings."

"That said, the definition of excess earnings is interesting," Mashuga says. "For example, if you bought rental real estate, income not deemed to be 'for occupation' can be excluded from your earnings." If you are planning to work past retirement, Mashuga recommends exploring the types of exempt income that won't reduce your Social Security benefits, such as investment earnings, dividends and capital gains.

3. What are the tax considerations?

Up to 85% of your Social Security benefits are subject to taxation by the federal government, and some states also tax Social Security income. "Additional earnings could affect the amount that is taxed, but good income planning may allow you to reduce or mitigate that impact," Mashuga says. "For example, if you have extra income and meet all the eligibility requirements, you may be able to use your employers' salary deferral plans or IRAs to reduce your taxable income."

Working past traditional retirement age might also put you in a different tax bracket than you had previously anticipated, so you'll want to make sure your portfolio is appropriately balanced between tax-deferred and taxable investments.

"In short, you'll want to sit down with your financial and tax advisors well in advance and look at your long-term picture," Mashuga says. "Taxes have become more complicated now, so it's best to look five or 10 years out for your retirement income distribution planning."

You may also access this article through our web-site http://www.lokvani.com/